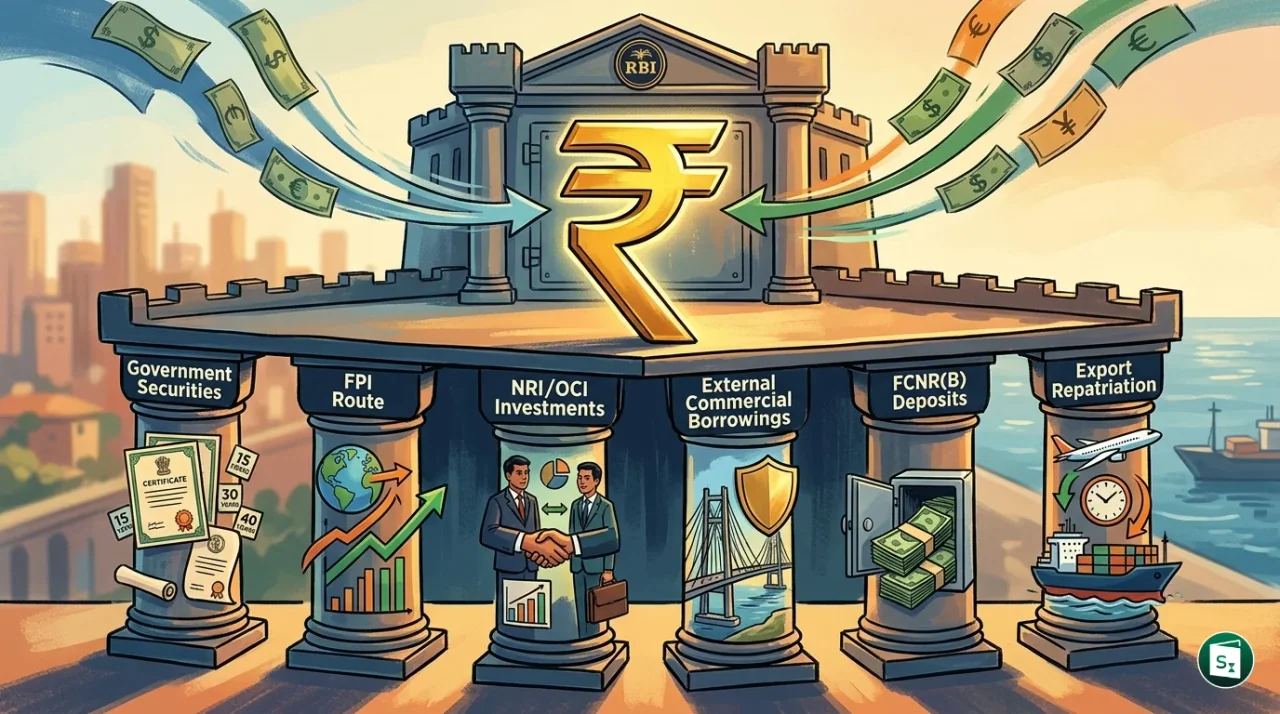

The Reserve Bank of India (RBI) has launched a comprehensive six-point policy package to encourage foreign capital inflows and stabilize the Indian rupee against global currency volatility. The intervention, announced alongside the central bank’s monetary policy review in June 2026, targets key channels of foreign investment including government securities, portfolio flows, non-resident deposits, and export proceeds. These coordinated measures aim to defend the currency and build external sector resilience amidst ongoing macroeconomic headwinds and geopolitical uncertainties.

Context of RBI’s Capital Inflow Package

The external sector of the Indian economy faced renewed pressure in early 2026 due to escalating geopolitical tensions in West Asia and a global risk-off sentiment. These developments led to sustained capital outflows by foreign portfolio investors, putting downward pressure on the Indian rupee and taxing the country’s foreign exchange reserves. In response, the Reserve Bank of India, established on April 1, 1935, under the Reserve Bank of India Act, 1934, and headquartered in Mumbai, coordinated a series of regulatory interventions to bolster foreign capital entry points.

Led by RBI Governor Sanjay Malhotra, the central bank designed the policy package to address structural bottlenecks in capital markets and incentivize foreign currency mobilization. These interventions aim to enhance dollar liquidity in the domestic market, providing a buffer against currency depreciation while supporting public infrastructure financing.

Opening Long-Term Bonds: Fully Accessible Route Expansion

To attract long-term stable foreign capital, the RBI expanded the scope of the Fully Accessible Route (FAR). Originally introduced in April 2020, the FAR framework enables non-resident investors to buy designated Government Securities (G-Secs) without any investment limits. Under the new guidelines, the central bank has added new central government securities with tenors of 15 years, 30 years, and 40 years to the designated list of specified securities under the FAR.

This expansion is designed to attract long-term yield-seeking foreign institutional investors, such as global pension funds and insurance companies. Furthermore, the RBI extended this route to cover Sovereign Green Bonds issued under these specific tenors. Sovereign Green Bonds are financial instruments created to fund projects with positive environmental impacts, and their inclusion under the FAR aligns India’s green transition with international capital markets.

Liberalising the General Route for Foreign Portfolio Investors

To optimize portfolio investment flows, the RBI has removed several restrictive regulations that foreign investors faced under the standard investment route. The central bank abolished historical entry bottlenecks under the General Route for Foreign Portfolio Investors (FPIs). FPIs represent investment groups or funds that hold financial assets in another country, and their activities are regulated by the Securities and Exchange Board of India (SEBI), which was established as a statutory body in 1992 under the SEBI Act, 1992, with its headquarters in Mumbai.

The three major restrictions removed by the RBI are:

- Short-term investment lock-ins: Regulations that previously restricted FPIs from holding debt instruments with residual maturities of less than one year.

- Concentration limits: Caps that restricted the maximum exposure an FPI could have to a single corporate group or entity.

- Individual security caps: Limits placed on the percentage of a single security issue that an FPI could purchase.

The elimination of these restrictions is designed to give FPIs greater operational flexibility, enabling quick adjustments to portfolio allocations in response to changing market dynamics.

Easing Equity Limits for NRI and OCI Investors

To attract retail-level capital from the Indian diaspora, the RBI has simplified the equity investment process for overseas individual investors. The central bank has increased the equity investment ceilings for Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) without requiring direct registration with SEBI. Additionally, the RBI extended this investment window to all individual Persons Resident Outside India (PROIs), placing them on par with NRIs and OCIs.

Before this policy change, overseas individual investors faced complex registration hurdles and lower investment ceilings under separate categories. Under the Foreign Exchange Management Act (FEMA), enacted in 1999 to consolidate laws relating to foreign exchange, individuals residing outside the country can now channel savings directly into listed Indian equities. By bypassing the requirement to register as a Foreign Portfolio Investor, the revised regulations reduce operational costs and compliance delays for individual cross-border retail investors.

Forex Swaps and Hedging Cost Support for Public Infrastructure and Deposits

To protect critical infrastructure sectors from forex fluctuations and to draw in foreign currency deposits, the RBI introduced two targeted financial mechanisms. First, a concessional foreign exchange swap facility was rolled out for External Commercial Borrowings (ECBs) raised by Central Public Sector Enterprises (CPSEs). External Commercial Borrowings are commercial loans raised by domestic entities from non-resident lenders, and Central Public Sector Enterprises represent state-owned companies in India. This swap facility insulates public infrastructure projects from foreign exchange volatility, stabilizing funding costs for essential capital works.

Second, the central bank announced that it will bear the full hedging costs for Authorized Dealer (AD) banks that raise fresh Foreign Currency Non-Resident (Bank) [FCNR(B)] deposits. These are foreign currency-denominated fixed deposits held by non-resident Indians in domestic banks. This special incentive applies to fresh deposits with maturities of three to five years and remains valid until September 30, 2026. By offsetting the hedging costs, the RBI reduces the cost of funds for domestic banks, making it highly competitive for them to raise foreign currency deposits and shore up national dollar reserves.

Restoring the Exporter Repatriation Timeframe

The final measure in the six-point package focuses on optimizing the inflows of foreign exchange earned through trade. The RBI has reduced the timeframe for exporters to realize and repatriate their international sales proceeds. The repatriation window has been shortened to nine months from the previous limit of 15 months.

Under export regulations, Indian businesses exporting goods and services must bring back foreign exchange earnings to India within a specified period and deposit them with an authorized dealer bank. The previous extension to 15 months was introduced to provide relief during periods of severe global trade disruption. By restoring the limit to nine months, the RBI aims to accelerate the conversion of overseas trade revenue into domestic bank deposits. This policy shift forces a quicker return of export earnings, immediately increasing dollar supply within the domestic forex market to support the exchange rate of the rupee.

Key Takeaways

- The Reserve Bank of India (RBI) was established on April 1, 1935, under the Reserve Bank of India Act, 1934, and is currently led by Governor Sanjay Malhotra.

- The RBI expanded the Fully Accessible Route (FAR), introduced in April 2020, to include new central government securities with tenors of 15, 30, and 40 years and matching Sovereign Green Bonds.

- Under the General Route, the RBI removed historical restrictions on Foreign Portfolio Investors (FPIs), including short-term investment lock-ins, concentration limits, and individual security caps.

- Investment ceilings for Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) were increased, and the facility was extended to all Persons Resident Outside India (PROIs) without SEBI registration.

- The RBI will bear the full hedging costs for Authorized Dealer (AD) banks raising fresh Foreign Currency Non-Resident (Bank) [FCNR(B)] deposits of three to five years until September 30, 2026.

- The realization and repatriation period for international sales proceeds earned by Indian exporters has been shortened to nine months from the previous 15-month limit.